𝐏𝐫𝐢𝐨𝐚𝐭𝐞 𝐃𝐞𝐝𝐭 𝐑𝐞𝐭𝐞𝐫𝐧𝐬: 𝐀𝐫𝐞 𝐀𝐥𝐩𝐡𝐚𝐬 𝐑𝐞𝐚𝐥?

The private debt asset class has been one of the fastest growing in recent years as investors were eager to capitalize on higher total returns. Various asset managers and finance companies rushed to offer closed-end funds and evergreen structures to capitalize on increased demand.

These funds usually provide mostly direct loans to firms that typically cannot get bank loans based on their creditworthiness. That is either due to already existing leverage, lack of assets, “creative” structure, or overall lower quality of the borrower. Thus, their cost of borrowing is higher.

The paper evaluates risk-adjusted returns of private debt funds from Burgiss-MSCI from 1992 to 2015. The dataset differentiates between generalists, mezzanine, distressed strategies, and small or large funds based on funds’ size.

Authors find that “private debt funds are also ‘equity-like’ both because their loans are substantially riskier than most other debt, and also because roughly 20 percent of their portfolios include equity features”. Therefore, the authors evaluate returns using both equity and debt benchmarks.

⬇️ 𝐎𝐭𝐡𝐞𝐫 𝐢𝐧𝐭𝐞𝐫𝐞𝐬𝐭𝐢𝐧𝐠 𝐩𝐢𝐞𝐜𝐞𝐬:

– Promised returns must be large enough to offset potential defaults and funds’ fees.

– Competition limits the extent to which funds can charge their rates.

– Fund investors earn only a rate of return appropriate for the risks they face, but no more.

⬆️ 𝐀𝐞𝐭𝐡𝐨𝐫𝐬’ 𝐟𝐢𝐧𝐝𝐢𝐧𝐠𝐬 𝐢𝐧 𝐧𝐞𝐦𝐝𝐞𝐫𝐬:

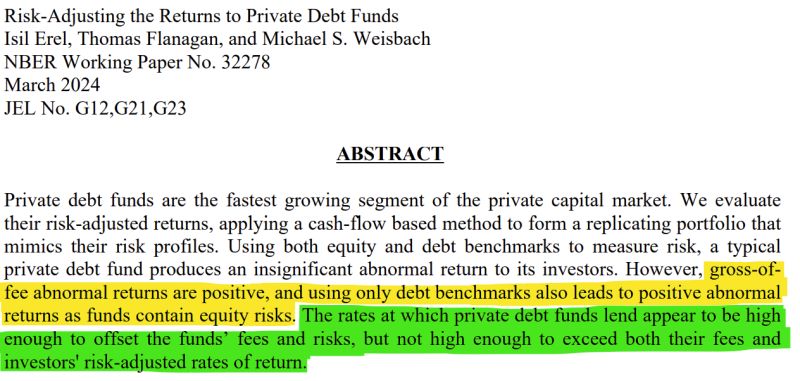

– On gross return bases, authors observe gross alphas of around 4%, almost equal to funds’ fees, i.e. management fee of 1.5% and 15-20% carried interest.

– If only the debt risk factor is used, risk-adjusted profit is positive and statistically significant (0.11$ on 1$ invested) and translates to 1.8% net alpha.

– Consistent with the above, positive and significant alphas on mezzanine and small funds, but no evidence of abnormal returns if equity factor is considered.

Authors conclude that private debt returns look more attractive than they actually are, because of the active equity risk factor. As always, selection is the key, and as evident from publicly traded debt instruments, there is significant variation in underwriting quality.

#PrivateDebt #alternativeInvestments #privateCredit #AssetAllocation

Leave a Reply